Manufacturing in a global oil crisis - A note from Uniplas

What is happening, and why does it matter?

March 2026 will be remembered as yet another moment, increasingly common in modern times, that exposes the fragility of global supply chains. The conflict involving the US, Israel, and Iran, along with the subsequent disruption in the Strait of Hormuz, has unsettled fuel markets and disrupted the movement of petrochemical feedstocks, polymers, and freight across the region. According to Reuters and AP, the Strait has been effectively closed to much of regular traffic, with shipping, energy, and export flows already under strain.

Why does this matter to plastic manufacturing in New Zealand?

For our industry, this matters immediately. Plastics NZ’s Middle East Petrochemical Disruption: Supply Chain Risk Assessment for New Zealand makes the point clear: this is no longer just an oil story, but a materials, freight, and manufacturing story. The report states that New Zealand is structurally exposed, as about 22% of our polymer supply comes directly from the Middle East and a further 56% comes from Asia (excluding China), much of which relies on Middle Eastern feedstocks and logistics. It also identifies PE and PP as the most exposed materials, with PVC and styrenics also vulnerable if disruption persists.

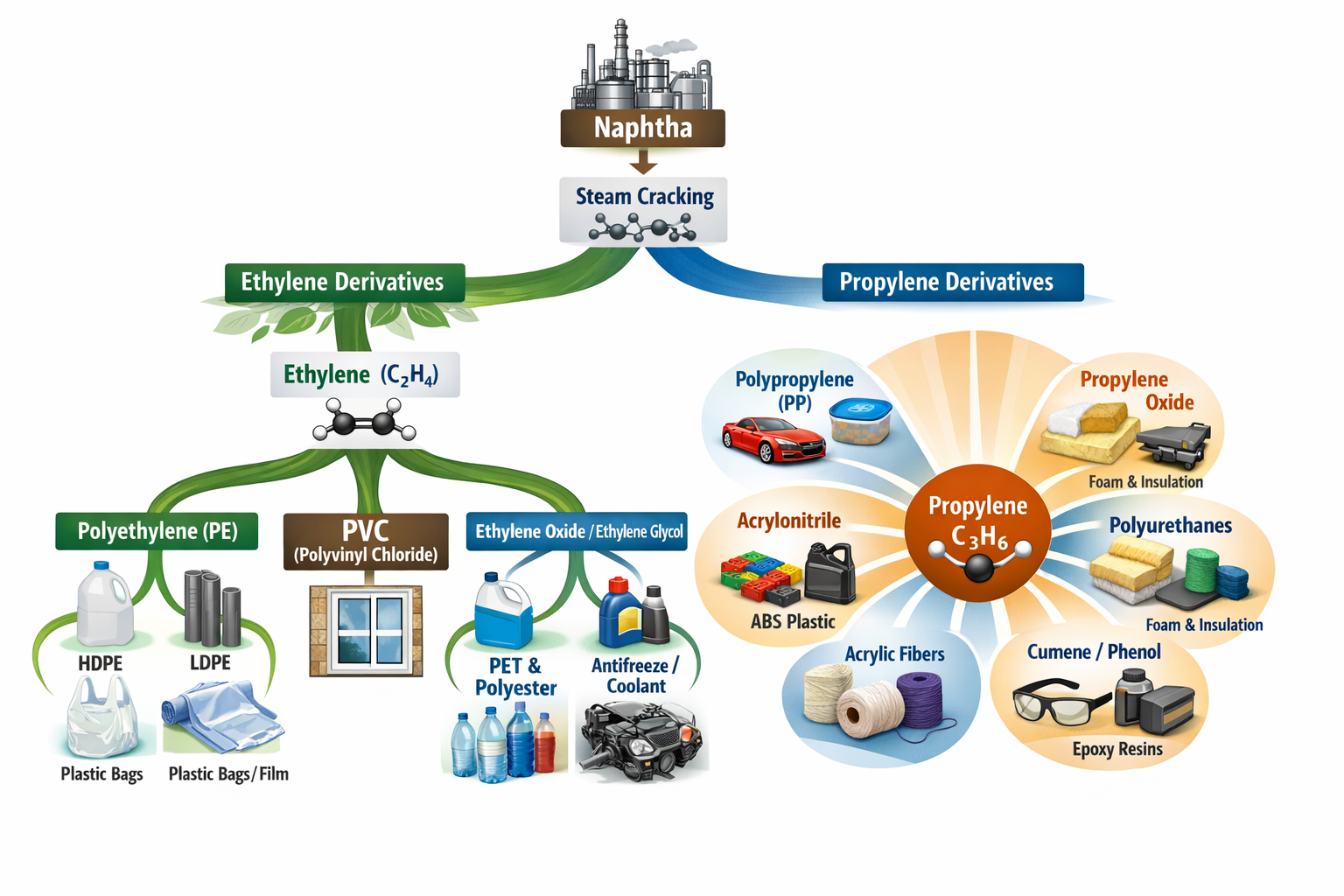

What is naphtha, and why does it matter?

Naphtha is one of the lighter fractions refined from crude oil. It sits in the barrel near petrol and ahead of heavier products like diesel. Unlike those, naphtha is mainly used as a petrochemical feedstock rather than a fuel. In steam crackers, naphtha is broken down into smaller building blocks such as ethylene and propylene gases, which are then polymerised to become plastics like polyethylene (PE) and polypropylene (PP).

Why has it affected PE, PP, and styrenics first?

PE and PP are predominantly produced in countries like Saudi Arabia and the UAE, where crude oil can be processed entirely from crude to plastic. This differs from other plastics, where the feedstock may originate from these countries, but the infrastructure and additional feedstock requirements may not be.

Can’t they just use the remaining 80% of the world’s oil to make this?

Conceptually, the oil is available to do this, but the complex chemistry and specific infrastructure required make the process difficult to start up elsewhere. Plants that produce millions of tonnes of plastic each year are typically designed to manufacture products with limited variability. The volumes, products, temperatures, feedstock, and additives would all require significant changes to the plant. Therefore, when the plants are unable to operate, export, or access naphtha, production cannot continue.

Why are some plastics more exposed than others?

Polycarbonate is a good example of how this risk works in practice. It is not as directly exposed to Gulf-origin finished resin as PE and PP, because New Zealand’s recent polycarbonate imports have mainly come from the rest of Asia, with smaller volumes from China, Europe, and North America, and no direct Middle Eastern volume shown in the Plastics NZ report for 2024-2025.

However, this does not mean polycarbonate is safe from supply risks. It is usually made from bisphenol A, which comes from phenol and acetone, and is turned into plastic through different chemical processes. Even if the final resin is shipped to New Zealand from Asia, Europe, or North America, it still depends on a complex global network of petrochemical materials.

The same broader point applies across the market. PE and PP are the most exposed materials for New Zealand because they sit at the centre of the Gulf-to-Asia petrochemical system and are closely tied to naphtha and LPG flows. That is why they tend to come under pressure first. By comparison, materials like nylon and polycarbonate often arrive in New Zealand from China, the rest of Asia, Europe, and North America, rather than directly from the Gulf, but supplies can still tighten if Asian feedstocks are constrained, shipping becomes unreliable, or overseas producers prioritise larger nearby customers over smaller distant markets like New Zealand.

How do I know if the material I use is at risk?

The lesson for all of us is straight forward. Complex global supply chains work well until they don’t. Once markets tighten, local relationships, early planning, and clear communication become more important than ever. Getting purchase orders in early gives everyone a better chance to secure materials, plan production properly, and protect continuity before shortages become apparent.

As a general rule, any material is more likely to be at risk if it relies heavily on imported resin, imported additives, long shipping routes, or overseas feedstock systems. Some materials are affected first, others later, but in a disrupted market, no polymer is completely insulated from the wider supply chain.

Doesn’t this just prove local supply chains matter more?

This does not contradict the value of local supply chains; in fact, it reinforces it. Local manufacturing still matters. Local warehousing still matters. Local relationships still matter. However, even in New Zealand, local conversion depends on imported resin, additives, freight capacity, and shipping reliability. The Plastics NZ report notes that many businesses here typically hold only around four to eight weeks of stock, which means resilience exists but only for a limited time. Once that buffer starts to diminish, the pressure shifts from higher pricing and limited offers to allocation, delayed replacement supply, and eventually operational strain.

Why do supplier relationships matter so much in times like this?

That is exactly why close supplier relationships matter most when markets stop behaving normally. In tight conditions, supply does not always flow to whoever asks last; it often goes first to committed customers, forward-planned work, and long-standing relationships. The report highlights material allocation, redirected shipments, short-dated offers, surcharges, and “no offer” situations already appearing in the market. In a small, distant market like New Zealand, staying close to your suppliers is not merely a nice to have it is one of the few practical tools you have.

Are prices really moving that fast?

We are already seeing this play out ourselves. In our own purchasing, some everyday materials have increased by about 56% in just a few days. That is a sharper move than most people are used to seeing in petrol, and it is a reminder that resin and packaging inputs can reprice very quickly when global supply tightens.

What should customers do now?

For customers, the message is simple: if you know a job is coming, get the purchase order in early. Early purchase orders give everyone a better chance to secure resin, plan production, hold stock against genuine demand, and reduce the risk of delay when supply becomes unreliable. They also help us make better decisions about what to prioritise, what to bring forward, and where to protect continuity for critical work.

How is Uniplas NZ responding?

At Uniplas NZ, we will continue to approach moments like this by staying close to our customers and suppliers and making early, sensible decisions while options are still available.

Where is this information coming from?

This note is informed by the Plastics NZ report Middle East Petrochemical Disruption: Supply Chain Risk Assessment for New Zealand (13 March 2026) and current Reuters/AP reporting on the conflict and Strait of Hormuz disruption.

Why choose Uniplas?

Made in

New Zealand

Local manufacturing ensuring quality control, Shorter lead times, and manufacturing transparency.

Sustainable manufacturing

Committed to environmental responsibility with one of NZ's largest rooftop solar installations and sustainable practices.

ISO 9001

certified

Internationally recognised quality management system ensuring consistent, high-quality output.

Engineering

expertise

Decades of injection moulding experience combined with advanced manufacturing capabilities.

Send us a message

We typically respond within 24 hours.

Our Business hours are : Mon-Fri, 9am-5pm

Taita, Lower Hutt

New Zealand